The Quiet Exit: What Scotiabank's Jamaica Buyout Reveals About Foreign Capital's New Playbook

When a 137-year presence decides to stop being a public company, the Caribbean should pay attention

By Janiel McEwan, Economist and Author

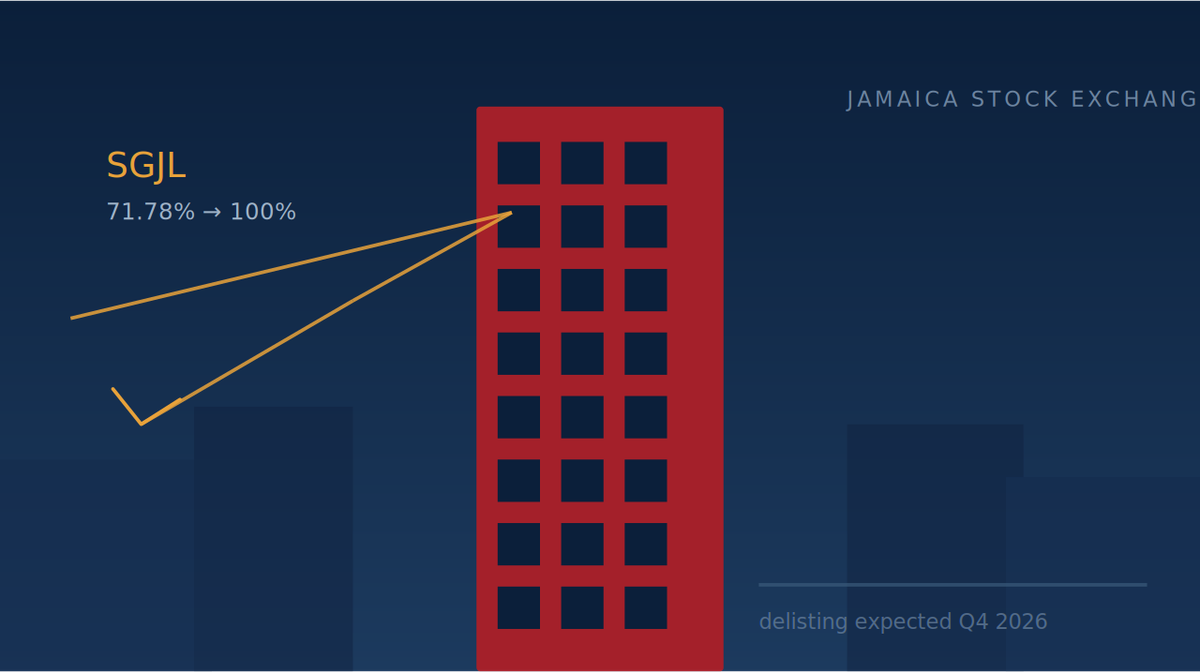

On June 12, 2026, Scotiabank announced it wants to buy out every remaining shareholder of Scotia Group Jamaica Limited and take the company private. The price tag: roughly J$61.50 per share, about US$0.5 billion in total, a 13% premium over recent trading. Subject to court and shareholder approval, by the end of this year, one of Jamaica's oldest and largest financial institutions could quietly disappear from the Jamaica Stock Exchange.

On the surface, this is a routine corporate transaction. Underneath, it's a story about who gets to own pieces of the Caribbean's economic future — and who decides that question.

The Deal, Stripped of Spin

Scotiabank's Caribbean holding company already controlled 71.78% of Scotia Group Jamaica. The proposal simply mops up the rest. The mechanism is a court-approved Scheme of Arrangement — a clean, efficient legal tool that requires minority shareholder approval but, once secured, forces a uniform outcome on everyone, including those who vote no.

The company's own language is instructive. This is about "capital and operational efficiency" and the ability to "respond more quickly to market opportunities." Translation: fewer disclosure obligations, no minority shareholders to negotiate with, and capital that can move across the bank's regional footprint without friction.

None of that is sinister. It's simply what a rational, profit-maximizing multinational does when a public listing has stopped paying for itself relative to the cost of compliance and governance overhead.

A Pattern, Not an Incident

Here's where it gets interesting for Jamaica specifically.

Scotia Group has traded on the JSE since the 1980s — one of the original anchor stocks that gave the exchange credibility as something more than a curiosity. Generations of Jamaican pension funds, NIS holdings, and individual investors built exposure to the banking sector partly through this single name.

Now consider the broader regional trend. Over the past decade, international banks across the Caribbean have been steadily retreating from retail banking — selling branches, exiting smaller markets, consolidating subsidiaries under tighter regional umbrellas. De-risking, the industry calls it. Each individual decision is defensible. The cumulative effect is a region where foreign financial institutions hold Caribbean market share with steadily diminishing local accountability structures attached to it.

A take-private of this scale isn't an aberration from that trend. It's the logical next step.

Why This Matters Beyond Wall Street Logic

For the Jamaica Stock Exchange, every blue-chip delisting is a depth problem. The JSE has earned real respect as an emerging-market exchange — strong returns, growing retail participation, increasing institutional interest. But an index is only as useful as the breadth of quality names it contains. Remove a heavyweight like Scotia Group, and the remaining float gets thinner, sector diversification narrows, and the exchange becomes more concentrated around the names that remain.

For local wealth creation, the math is straightforward and uncomfortable. A 13% premium is a fine short-term outcome for shareholders cashing out today. But it's also the closing of a door — one fewer vehicle through which an ordinary Jamaican, through a pension fund or a brokerage account, can hold an ownership stake in one of the institutions that processes their salary, holds their mortgage, and shapes their access to credit.

For governance, a listed company carries obligations: independent directors, public financial disclosure, an annual general meeting where shareholders — however small — can ask questions. A privately held subsidiary answers to one shareholder, headquartered abroad. The bank insists there will be "no material impact on operations." That may well be true in the near term. But the accountability architecture changes permanently, and that's not nothing.

The Counterargument Deserves Its Due

It would be intellectually dishonest to frame this only as loss.

From Scotiabank's perspective, this is sound capital management. Minority shareholders introduce friction — disclosure costs, governance requirements, the need to justify capital allocation decisions to outside parties who may not share the parent company's regional strategy. Removing that friction allows faster decision-making in a market where conditions can shift quickly.

From some minority shareholders' perspective, this might genuinely be a good outcome. If you didn't believe SGJL's share price had significant further upside, a 13% premium with a guaranteed cash exit is more attractive than continuing to hold an illiquid position in a thinly traded local stock. Not every shareholder wants long-term exposure — some want liquidity, and this delivers it.

The independent directors' unanimous recommendation also can't be dismissed outright. Whatever the power dynamics of negotiating with a 71.78% shareholder, a complete rejection of any premium in favor of the status quo isn't obviously the better outcome for everyone either.

The Human Impact, Honestly Assessed

For the depositor walking into a branch in Mandeville or Half-Way Tree, almost nothing changes immediately. Same accounts, same staff, same services. Scotia Group remains regulated by the Bank of Jamaica regardless of its listing status; deposit protections through the JDIC are untouched.

The impact is slower and more structural. It's about where decisions get made, how much public information exists about one of the country's largest financial institutions, and whether the next generation of Jamaican investors has one fewer blue-chip option when they're building a portfolio.

What Policymakers Should Be Asking

This single transaction doesn't require a regulatory response — it's a lawful, disclosed, court-supervised process. But it should prompt a broader conversation that Jamaica's financial policymakers have been circling for years without quite landing on:

First, what is the JSE's strategy for pipeline — not just attracting new listings, but creating conditions where companies want to stay listed rather than viewing a public float as a temporary inconvenience? Listing requirements, minority shareholder protections, and the cost-benefit calculus for issuers all deserve scrutiny.

Second, is there a role for local institutional investors — pension funds, the NIS, sovereign wealth-style vehicles — to take a more active stake in transactions like this, not to block them, but to ensure Jamaican capital has a seat at the table when foreign parents make consolidation decisions?

Third, as Caribbean banking continues to consolidate under fewer regional players, does Jamaica's regulatory framework need sharper tools for monitoring concentration risk and governance quality in systemically important institutions that are no longer subject to public market discipline?

These aren't questions with easy answers. But they're questions worth having before the next take-private, not after.

The McEwan Insight

There's a temptation to read this transaction as either entirely benign — "just business" — or entirely alarming — "foreign capital extracting value and leaving." Both framings are too simple.

The more accurate reading is this: Jamaica's capital markets are at a structural inflection point. For decades, the JSE's credibility was built partly on the presence of large, recognizable, foreign-anchored names that gave local investors exposure to institutions with regional scale. That model is now quietly reversing — not through crisis, but through the routine, lawful exercise of majority shareholder rights.

The question isn't whether Scotiabank is doing anything wrong. It's whether Jamaica's capital market architecture is evolving fast enough to replace what's being lost — with homegrown listings, deeper local institutional participation, and governance structures that don't depend on foreign parents choosing to stay public.

If the answer is no, then transactions like this one won't be isolated stories. They'll be the new normal — and the JSE of 2030 could look meaningfully thinner than the JSE of today, one rational corporate decision at a time.

Where This Leaves Us

Scotia Group Jamaica's shareholders will vote in the coming months. Whatever they decide, the bank's branches will stay open, its staff will keep working, and most Jamaicans will notice nothing different on the surface.

But beneath that surface, a quiet recalibration is underway — about who owns the Caribbean's financial institutions, who gets a say in how they're run, and whether "emerging market" status is something Jamaica's capital markets are building toward, or slowly drifting away from.

The companies that choose to stay listed — and the ones Jamaica manages to attract or build from scratch — will say more about the next decade of this economy than any single earnings report ever could.

Janiel McEwan is an economist and author writing on Jamaican and Caribbean economic policy. The McEwan Index.